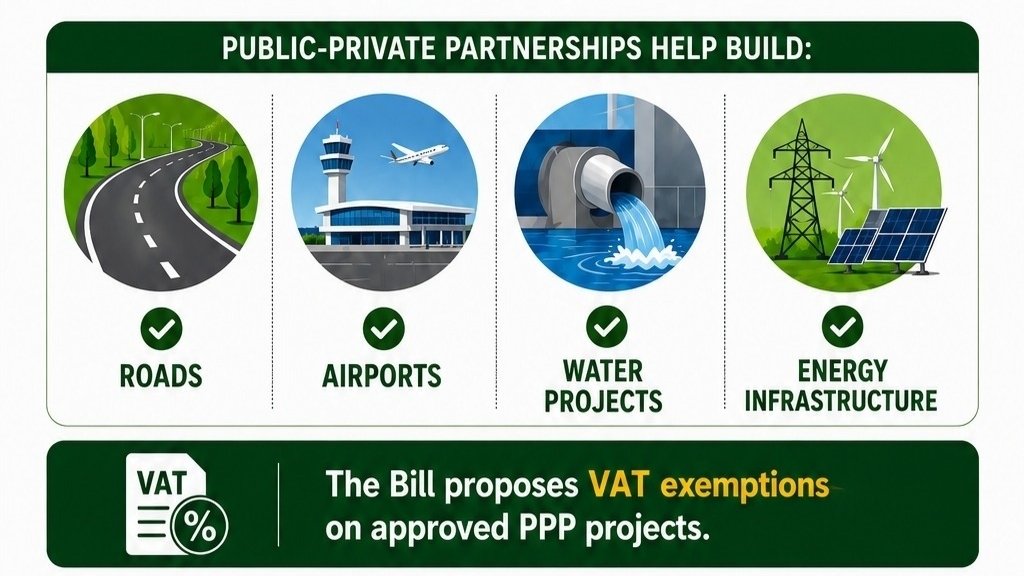

The Finance Bill 2026 proposes an exemption from value added tax on goods and services supplied directly and exclusively for approved public-private partnership projects.

This provision would apply once projects receive formal clearance through established processes involving the PPP Committee and relevant government bodies. Private partners would benefit from the removal of the 16 percent tax on qualifying inputs such as construction materials and specialist services.

Public-private partnerships have gained traction in Kenya as a way to tackle large funding gaps in infrastructure. Under these models, private entities typically take on financing, construction and operation responsibilities in return for long-term revenue streams.

Kenya has seen several high-profile examples. The Nairobi Expressway, developed with a Chinese partner, has changed commuting patterns in the capital although it continues to draw comment over toll levels and contract terms.

Road upgrades remain a focus area. Work on the Nairobi-Nakuru-Mau Summit Highway has proceeded with private sector involvement aimed at improving connectivity along that key route.

Energy projects have also featured PPP arrangements. Geothermal developments in the Menengai area have attracted investment through such frameworks. Similar approaches appear in water sector plans, including proposals for desalination plants on the coast.

The exemption requires formal approval from the Cabinet Secretary for the National Treasury following recommendations from the responsible line ministry and the PPP Committee.

Questions have arisen around how the system would work in practice. Legal and industry observers have called for strong eligibility checks, verification procedures and post-project audits to prevent any spillover of tax relief into unrelated activities.

The country holds an active pipeline of PPP initiatives across transport, energy, water, housing and health. Outcomes so far have been mixed. Some projects have moved forward relatively smoothly while others have faced delays, cost pressures or public debate over terms.

This VAT measure forms one part of broader changes in the bill. Other adjustments address areas such as pharmaceutical supplies, animal feed components and electric vehicles.

Stakeholders from the construction sector and civil society groups are paying close attention. They have highlighted the importance of clear governance frameworks to protect government revenue while encouraging genuine infrastructure investment.

Parliament will continue scrutiny of the bill in coming weeks. Amendments could still alter the final wording of the clause.

If passed in its current form the exemption would take effect from July 2026. Kenya continues to grapple with significant infrastructure needs driven by population growth and economic expansion. Private participation through PPPs has become one established route for addressing those demands.

This article is not sponsored.

Comments (0)

Leave a Comment

No comments yet. Be the first to share your thoughts!