A brand new commercial haulage vehicle purchased through a local bank asset financing arrangement has suffered a severe road accident within just weeks of its deployment. This unexpected incident highlights the immense vulnerabilities faced by independent logistics and construction transport investors in Kenya.

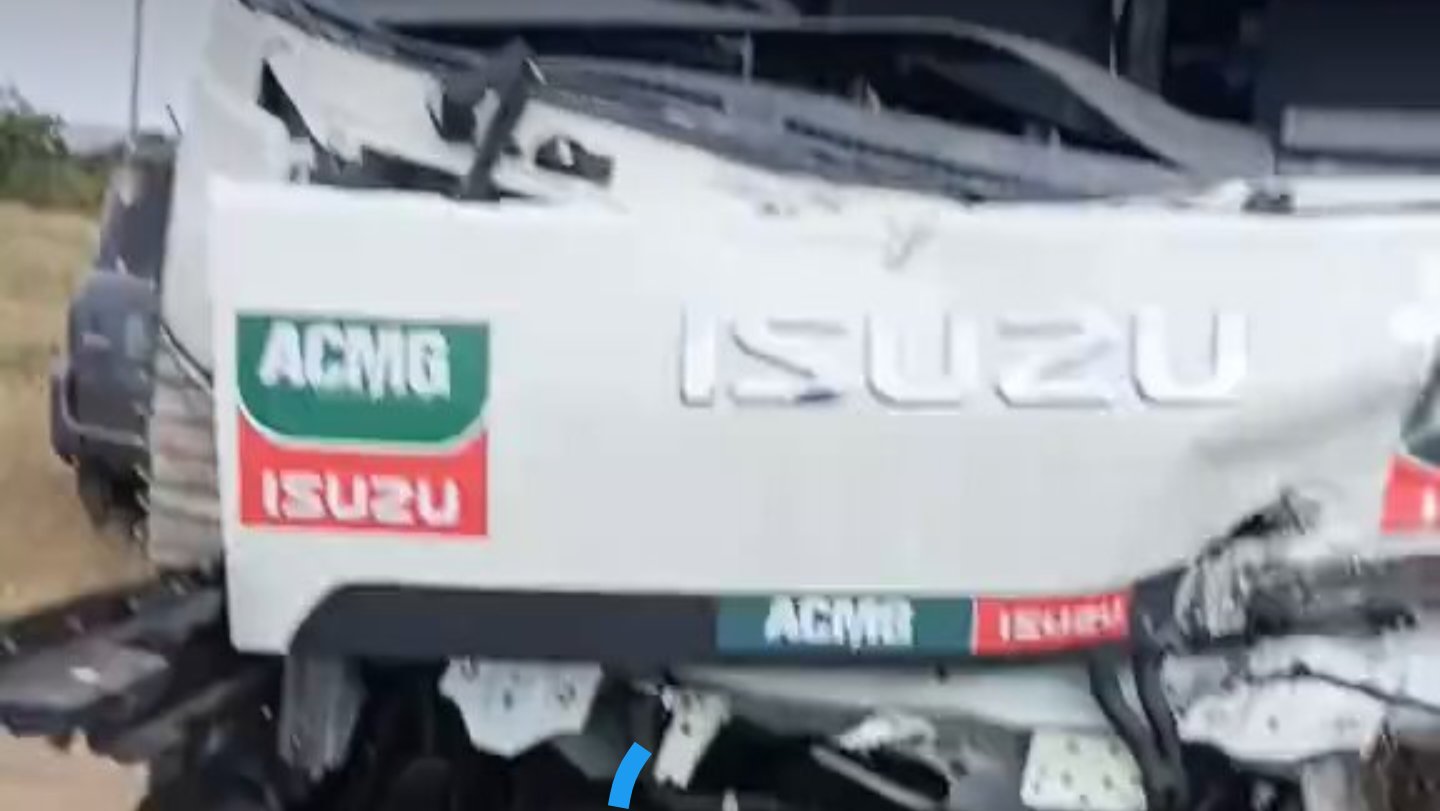

The vehicle involved in the crash, which was an Isuzu commercial truck supplied by the Africa Commercial Motor Group Limited (ACMG), was operating under a structured credit agreement. The severe structural damage to the cabin indicates a high-impact collision, which has effectively rendered the asset completely non-operational.

Haulage and construction logistics operators face immense financial pressure, when newly acquired assets suffer extensive physical damage before generating any meaningful returns. The loss of a primary operating unit immediately halts income generation, while the underlying financial liabilities remain active.

A standard asset financing plan for these popular medium-duty commercial units typically requires a substantial initial cash deposit of five hundred thousand Kenya Shillings. This initial payment represents a significant portion of working capital for small enterprises, who operate within the transport sector.

This upfront capital commitment is usually accompanied by a temporary three-month grace period designed to let the business establish stable routes before installments commence. However, if a catastrophic accident occurs during this brief window, the financial planning of the business is severely disrupted.

For many independent transport operators across Kenya, the subsequent monthly remittance stands at ninety thousand shillings over a fixed multi-year term. Meeting these steep monthly obligations becomes nearly impossible, when the vehicle is sitting in a yard completely destroyed rather than hauling construction materials.

The near-total destruction of a commercial truck before the completion of its first month on the road creates immediate and severe financial distress. Owners find themselves in a precarious position, where they must navigate complex insurance investigations while trying to manage persistent bank loan demands.

Industry experts note that comprehensive commercial auto insurance policies can take several months to investigate, assess, and finally settle claims for written-off logistics assets. During this protracted administrative interim, the vehicle owner receives no revenue, but remains legally bound to the asset financier.

Meanwhile, local financial institutions expect consistent repayment schedules regardless of the actual operational status or physical condition of the financed vehicle. This rigid structure means that an investor could be forced to pay monthly installments, although the asset no longer functions.

The recent registration sequence of the wrecked vehicle confirms that the commercial unit was a brand new entry into the competitive local transport market. Such early-stage operational losses severely disrupt the delicate cash flow balances, which small logistics businesses rely upon to remain solvent.

Transport sector stakeholders are increasingly calling for more flexible asset protection measures, including specialized loan repayment restructuring from local financing institutions. They argue that traditional insurance policies do not adequately protect the cash flow of an entrepreneur, when a severe crash occurs.

Authorized dealerships like ACMG provide standard technical support, but physical safety on Kenyan roads remains entirely under driver control. Comprehensive driver training programs and modern fleet oversight systems are critical components, which investors must prioritize to reduce these devastating operational risks on public highways.

Comments (0)

Leave a Comment

No comments yet. Be the first to share your thoughts!